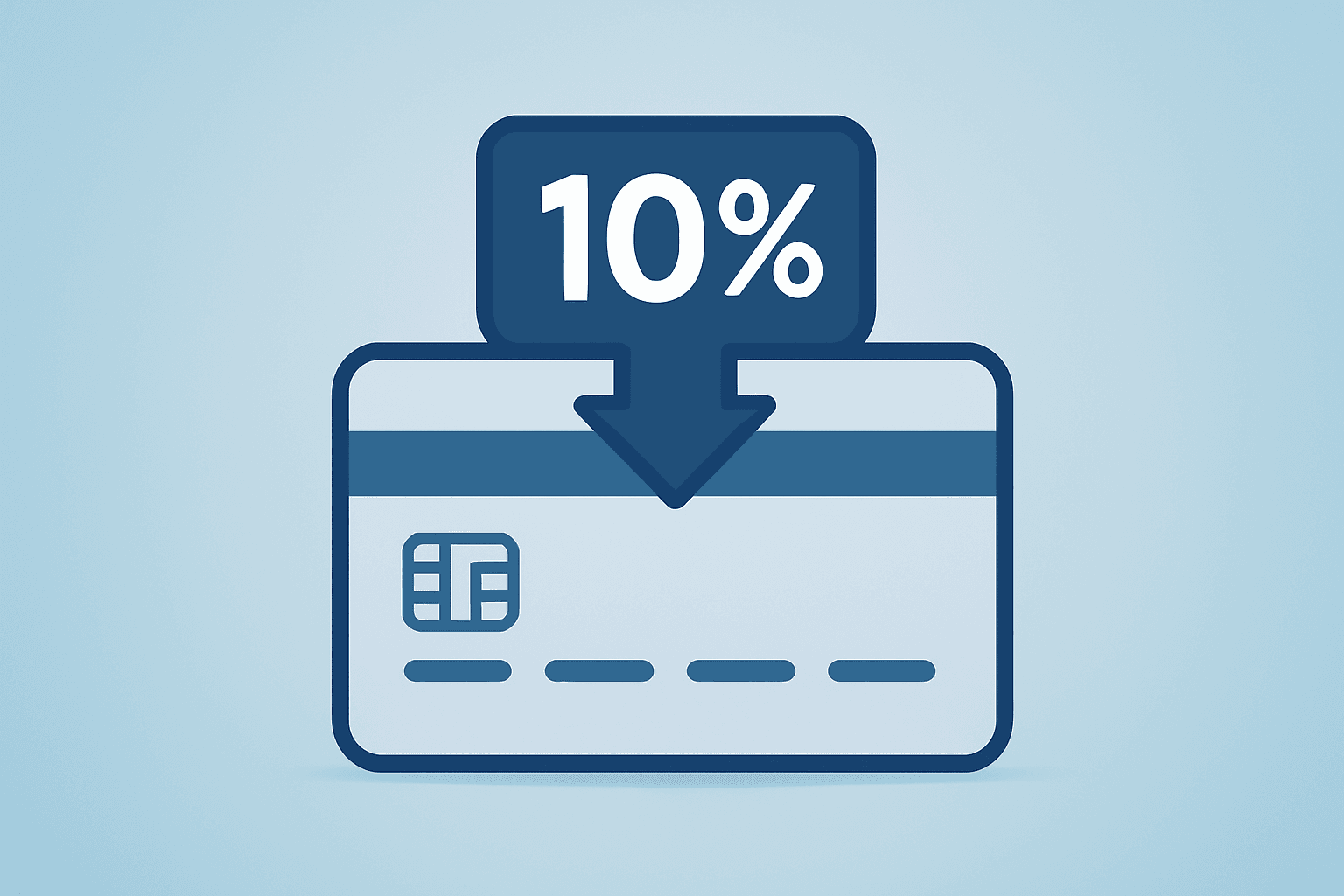

Trump 10% Credit Card Cap Clouds Bank Stocks

Trump 10% Credit Card Cap proposal would take effect Jan. 20; trade groups warn credit squeeze and analysts flagged headline risk for card issuers.

KEY TAKEAWAYS

- A one-year 10% credit-card APR cap would begin Jan. 20 as proposed.

- Bank trade groups warned the cap would reduce credit availability and push borrowers toward costlier alternatives.

- Analysts called it a policy and headline risk for card issuers but judged enactment unlikely.

HIGH POTENTIAL TRADES SENT DIRECTLY TO YOUR INBOX

Add your email to receive our free daily newsletter. No spam, unsubscribe anytime.

Former President Donald Trump proposed a one-year 10% cap on credit-card interest rates starting January 20, 2026, in a Truth Social post on January 9. He did not specify how the cap would be enforced. Banking trade groups warned the measure could reduce credit availability, creating a headline risk for card issuers.

Proposal and Timing

Trump announced the credit card annual percentage rate (APR) cap as relief for Americans facing rising revolving credit balances. The proposal calls for a one-year limit on consumer credit-card interest rates beginning January 20. The announcement did not include details on how the administration would compel card issuers to comply. Previous efforts to impose interest-rate caps on credit cards have struggled to gain traction in Congress, highlighting the challenges of passing such legislation.

Industry Reaction and Market Risks

The American Bankers Association and four other banking trade groups issued a joint statement opposing the cap. They argued it would reduce credit availability and harm consumers and small businesses, saying, "If enacted, this cap would only drive consumers toward less regulated, more costly alternatives." The groups added they share the goal of expanding access to affordable credit but oppose this specific approach.

Market commentary flagged potential earnings pressure for card issuers and noted that bank stocks were bracing for impact. Analysts described the proposal as a policy and headline risk, though some, including Jefferies, view enactment as highly unlikely. A review of the 72-hour window found no filed federal legislation, executive order, or regulatory proposal implementing the cap, nor new rules or guidance from federal banking regulators tied to the pledge.

If implemented, analysts say lenders could tighten underwriting, reduce credit lines, or shift fees and rewards to offset lost interest income. No credit card issuers or payment networks, including American Express, Capital One, Mastercard, or Visa, have issued public statements or SEC filings addressing the proposal.